The financial landscape is undergoing a fundamental transformation as crypto vs traditional banking becomes a central debate in modern commerce. Understanding the core differences between blockchain-based systems and conventional banking infrastructure is essential for businesses and individuals evaluating payment methods. This analysis examines transaction speed, cost structures, security frameworks, and operational accessibility to provide clarity on how these two systems compare.

Traditional banking has dominated financial transactions for decades through established networks like SWIFT, ACH, and card processors. Meanwhile, cryptocurrency and blockchain technology promise decentralized, transparent, and efficient alternatives. The question is no longer whether digital assets will play a role in payments, but rather which system best serves specific business requirements.

Understanding Traditional Banking Systems

Traditional banking operates through centralized institutions that act as intermediaries for all financial transactions. Payments pass through multiple layers of verification involving banks, clearing houses, and payment processors. This centralized model provides established regulatory oversight, consumer protections, and dispute resolution mechanisms refined over generations.

The infrastructure includes wire transfers, credit and debit card networks, and automated clearing houses. Banks maintain customer deposits, verify identities, monitor for fraud, and ensure compliance with anti-money laundering regulations. This centralized control creates stability and trust, but introduces delays and costs at each intermediary layer.

Key Features of Traditional Banking

- Centralized control through regulated financial institutions

- Established consumer protection mechanisms, including deposit insurance

- Transaction reversibility through chargebacks and dispute processes

- Comprehensive fraud monitoring and identity verification

- Integration with existing business and accounting systems

- Regulatory compliance frameworks with clear legal precedents

How Cryptocurrency Payment Systems Operate

Cryptocurrency payments leverage blockchain technology to enable peer-to-peer transactions without traditional intermediaries. When a user initiates a crypto payment, it is broadcast to a decentralized network that verifies and records it on a public ledger, eliminating the need for banks to validate each transaction.

Blockchain payment systems utilize cryptographic algorithms to secure transactions and maintain an immutable record of all transfers. Smart contracts can automate payment execution based on predefined conditions, enabling programmable money. Users maintain control of their assets through private keys rather than relying on third-party custodians.

Core Characteristics of Crypto Payments

- Decentralized networks operating without central authorities

- 24/7 availability with no banking hours or holidays

- Transparent transaction records on public blockchains

- Programmable payments through smart contract integration

- User-controlled custody through private key management

- Global accessibility requires only internet connectivity

Stablecoins vs Traditional Payments: Speed Comparison

Transaction settlement time represents one of the most significant differentiators between these systems. Traditional banking infrastructure processes domestic payments with settlement times ranging from instant (on networks like FedNow, RTP, and SEPA Instant) to one or two business days for ACH transfers. International wire transfers typically require one to five business days due to correspondent banking chains.

Crypto payments, particularly stablecoins, settle in seconds to minutes regardless of geographic location. The blockchain operates continuously without weekend or holiday interruptions, enabling round-the-clock transaction finality. This speed advantage becomes particularly pronounced for cross-border payments, where traditional systems must navigate multiple intermediaries and time zone constraints.

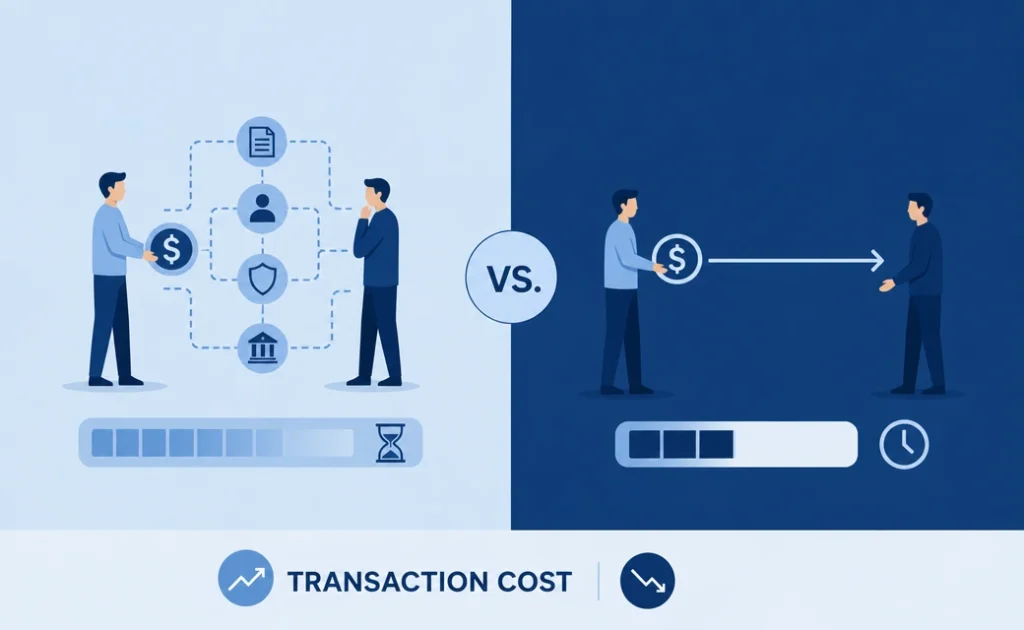

Transaction Cost Structure Comparison

Fee structures reveal another fundamental difference. Cross-border wire transfers through SWIFT networks typically incur fees ranging from fifteen to fifty dollars or more, with additional correspondent bank charges and foreign exchange spreads. Retail customers often face FX markups between two and five percent, while institutional clients may secure spreads of 0.5 to 1.5 percent.

Blockchain transactions generally cost between one cent and five dollars, depending on network congestion. Stablecoins transferred through institutional OTC channels experience minimal FX spreads (0 to 0.5 percent) compared to traditional banking markups. These cost savings compound significantly for businesses processing high volumes of international transactions.

| Cost Factor | Traditional Banking | Cryptocurrency |

| Domestic Transfer Fee | $0-$30 (depending on method) | $0.01-$2 |

| Cross-Border Transfer Fee | $15-$50+ per transaction | $0.01-$5 |

| FX Spread (Retail/SMB) | 2-5% | 0-0.5% |

| FX Spread (Institutional) | 0.5-1.5% | 0-0.5% |

Security and Risk Management

Security models differ fundamentally between centralized and decentralized systems. Traditional banks employ centralized fraud monitoring, identity verification procedures, and deposit insurance programs that protect consumers up to regulatory limits. Transactions can be reversed through chargeback mechanisms, and established legal frameworks provide recourse for disputes.

Cryptocurrency systems distribute security across network participants, using cryptographic protection for each transaction. However, users bear responsibility for private key custody, and transactions are generally irreversible once confirmed. This model eliminates counterparty risk associated with bank failures but introduces personal responsibility for security practices. Lost or stolen cryptocurrency typically cannot be recovered through institutional guarantees.

Comparison of Traditional Payments and Blockchain Technology

When evaluating these systems across multiple dimensions, distinct patterns emerge. Blockchain excels in cross-border transaction speed, cost efficiency, and 24/7 availability. Traditional banking maintains advantages in regulatory maturity, consumer protections, and integration with existing business workflows. The optimal choice depends on specific transaction characteristics rather than one system universally outperforming the other.

Use Case Applications

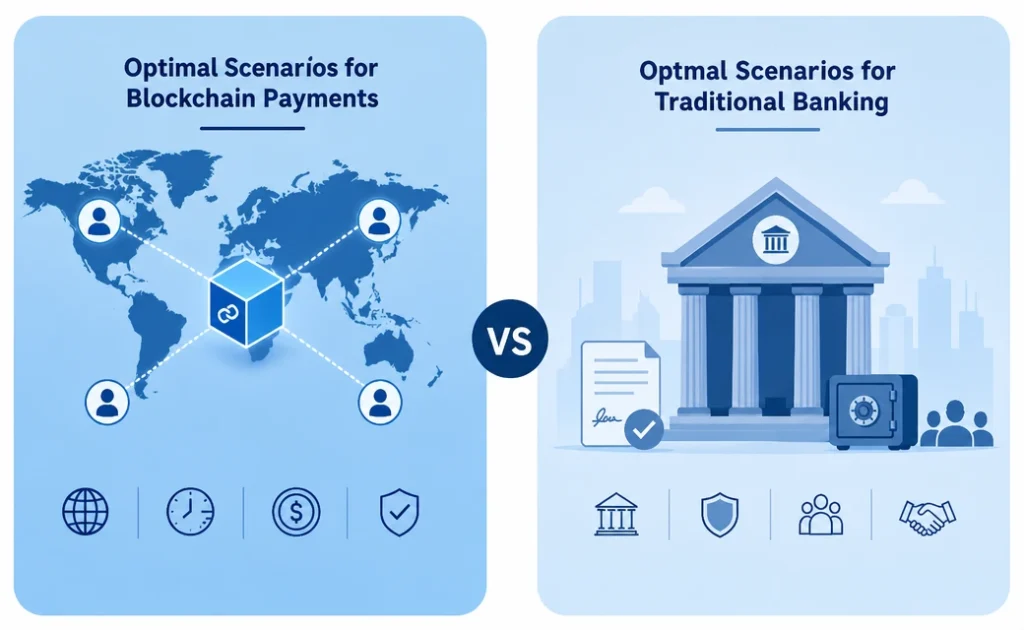

Different transaction scenarios favor different systems based on their inherent characteristics. Cross-border business-to-business payments benefit significantly from blockchain’s speed and cost advantages. Treasury operations requiring 24/7 liquidity access align well with cryptocurrency’s continuous availability.

Domestic retail transactions, recurring payments, and scenarios requiring consumer protection mechanisms remain well-served by traditional banking infrastructure. Businesses with established accounting systems and regulatory compliance requirements often find traditional rails easier to integrate and audit.

Optimal Scenarios for Blockchain Payments

- International B2B transfers requiring rapid settlement

- Micropayment systems where traditional fees prove prohibitive

- Programmable payments triggering automated business logic

- 24/7 treasury operations without banking hour constraints

- Transparent supply chain payments requiring audit trails

Optimal Scenarios for Traditional Banking

- Domestic consumer transactions with chargeback protection

- Recurring subscription payments integrated with existing systems

- Credit-based transactions require a lending infrastructure

- Large-value transactions requiring formal documentation

- Payroll processing with tax withholding and reporting requirements

- Regulatory compliance in heavily regulated industries

Implementation Considerations for Businesses

Organizations evaluating payment infrastructure options must assess technical readiness, regulatory positioning, and strategic alignment. Cryptocurrency integration requires wallet management capabilities, private key custody solutions, and volatility mitigation strategies. Businesses must develop internal expertise or partner with specialized service providers to manage blockchain transactions securely.

Hybrid approaches increasingly offer practical solutions, combining traditional banking stability with blockchain efficiency. Payment processors now provide APIs that convert cryptocurrency to fiat currency at settlement, eliminating volatility exposure while maintaining blockchain speed advantages.

Frequently Asked Questions

- Are crypto payments faster than traditional bank transfers?

Cryptocurrency payments typically settle in seconds to minutes, regardless of location, operating 24/7. Traditional domestic instant payment rails like FedNow and SEPA Instant match blockchain speeds, but international wire transfers require one to five business days. Blockchain maintains consistent performance without banking hours limitations.

2. Which system offers lower transaction fees?

Blockchain transactions generally cost $0.01 to $5, while cross-border wire transfers range from $15 to $50 or more. Stablecoins vs traditional payments show significant differences in FX spreads, with crypto offering 0-0.5% compared to traditional banking’s 2-5% for retail customers.

3. Is cryptocurrency more secure than traditional banking?

Security models differ fundamentally. Traditional banking provides deposit insurance, fraud monitoring, and transaction reversibility. Cryptocurrency offers cryptographic security and eliminates counterparty risk, but requires users to manage private keys. Lost crypto typically cannot be recovered through institutional guarantees.

4. Can businesses use both payment systems simultaneously?

Yes, hybrid approaches combining traditional banking stability with blockchain efficiency are increasingly common. Payment processors offer APIs that convert cryptocurrency to fiat at settlement, allowing businesses to access blockchain advantages without abandoning established financial infrastructure.

5. What are the main advantages of traditional banking over crypto?

Traditional banking excels in regulatory maturity, consumer protection mechanisms, transaction reversibility, and integration with existing business systems. It provides established dispute resolution processes, deposit insurance, and comprehensive compliance frameworks that cryptocurrency systems currently cannot fully replicate.